Sale of products and services is the main revenue stream for most of the businesses and its maximization is, therefore, one of the prime objectives of commercial entities. Similarly, purchase of products, both tradable goods and raw material, or expenditures on provision of services is the main expense category for them.

Commercial entities operate for profit which necessitates them to minimize their expenses as far as possible so as to maximize their profit margin. Discount is a reduction in the cost/price of any goods or services that are sought to be sold. In a bid to increase sales, several sellers offer discounts to their customers to make the sales price more attractive. At the same time, buyers negotiate discounts with their suppliers to reduce their cost of goods/services.

This article looks at meaning of and differences between two ends of the discount spectrum – discount allowed and discount received.

Definitions and meanings

Discount allowed

Discount allowed is the reduction in sales price of the goods or services sought to be sold, that is offered by the seller to the buyer. It becomes an expense for the seller as it reduces the receivable value of the sale transaction.

Discount allowed is of two types; it can be either a trade discount or a cash discount. A trade discount is generally offered at the time of a sale transaction for promoting bulk sales. A cash discount, on the other hand, is offered after the conclusion of the sale transaction to encourage early payment by the buyer.

Example

Roberts Inc. is a trader that sells office furniture. Johnson, who is a professional, purchases 30 office chairs from Roberts for his office on January 01, 2021. The gross selling price of each chair is $100 and a trade discount of 10% is offered with a credit period of 30 days. After 10 days on January 11, Roberts further offers a cash discount of 3% if the buyer makes immediate payment for the sale. Johnson accepts the offer and makes the payment immediately on the same day.

Roberts Inc. would record the journal entries for the sale and receipt of payment as follows:

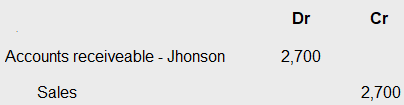

Journal entry for the sale of 30 chairs to Johnson on account:

Trade discount allowed in above sale transaction is $300 (= 30 × $100 × 10%). This discount is not recorded separately in the books of accounts; hence, Roberts Inc. would record this sale transaction at its net value of $2,700 as computed below:

Net value of sale transaction = (30 chairs × $100) – ($300 trade discount)

= $3,000 – $300

= $2,700

On January 01, 2021, Roberts Inc. would make the following journal entry to record the sale of 30 chairs:

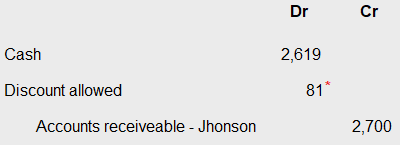

Journal entry for the receipt of payment from Johnson:

The cash discount allowed is realized and recorded in the books of seller at the time of actual receipt of payment from the buyer. It is seller’s expense and is, therefore, debited to his profit and loss account.

On January 11, 2021, Roberts Inc. would record the receipt of payment from Johnson by means of the following journal entry:

*Cash discount allowed: $2,700 × 0.3 = 81

Discount received

Discount received is the reduction in purchase price received by the buyer, on the goods bought or services availed from the seller. It becomes an income for the buyer as it reduces the amount payable towards the expense of goods purchased or services consumed.

Discount received can also be either a trade discount or cash discount. A trade discount is negotiated and received at the time of purchase of goods or services and is generally granted to the buyer to encourage and promote the bulk deals. It is not separately accounted for in the books of the buyer.

Cash discount is availed by the buyer generally for making an early payment against the settlement of a previous credit purchase of inventory or service.

Example

Continuing the example above, the accounting entries to record the purchase of chairs and payment thereof are presented below:

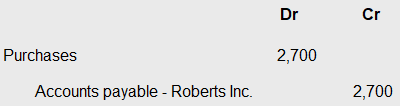

Journal entry for the purchase of 30 chairs from Roberts Inc. on account:

Similar to Roberts Inc., Johnson would not separately account for the trade discount received but would record the purchase transaction at its net value of $2,700 (= $3,000 – $300).

Johnson’s journal entry to record the purchase of 30 chairs on January 01, 2021 is as follows:

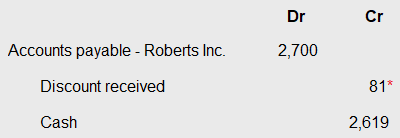

Journal entry for making the payment to Roberts Inc:

The cash discount received is realized and brought in the books of buyer at the time of making payment to the seller. It is buyer’s income and is, therefore, credited to his profit and loss account.

Johnson would record the payment made to Roberts Inc. on January 11, 2021 through the following journal entry:

*Cash discount received: $2,700 × 0.3 = 81

Difference between discount allowed and discount received

The seven key points of difference between discount allowed and discount received have been listed below:

1. Meaning

- Discount allowed is the concession in sales price granted by the seller to the buyer on sale of goods/services.

- Discount received is the concession in purchase price enjoyed by the buyer on purchase of goods/services from a seller.

2. Impacts

- Discount allowed goes to reduce the sales price for the seller or the payment received against sales by the seller.

- Discount received goes to reduce the purchase price for the buyer or the net amount payable against such purchases by the buyer.

3. Nature of the account

- Discount allowed is an expense ledger account.

- Discount received is an income ledger account.

4. Accounted in books of

- Discount allowed is recorded in the books of the seller of goods/services.

- Discount received is recorded in the books of the buyer of goods/services.

5. Accounting manner

- Discount allowed is debited to the profit and loss account of the seller.

- Discount received is credited to the profit and loss account of the buyer.

6. Benefits

- Discount allowed can be beneficial to the seller as it can increase the volume of sales by attracting customers towards discounted prices. It can also prepone the seller’s cash inflow, thus saving on interest cost when discount allowed results in early payment by the creditor.

- Discount received is beneficial to the buyer as it reduces his cost of goods/services.

7. Drawback

- The drawback of discount allowed to the seller is that it reduces his cash inflow for the particular sales transaction thereby decreasing his profitability per transaction as well.

- The drawback of discount received for the buyer (in case of cash discount) is that it prepones his cash outflow on goods or services purchased.

Conclusion

Both discount allowed and discount received are essentially two sides of the same sale/purchase transaction. They both impact cash flow – discount allowed has a negative impact on cash flow of the seller in that it reduces his cash inflow whereas discount received has a positive impact on the cash flow of the buyer as it reduces his cash outflow.

Conclusion of sale and purchase transactions have many parameters but one key parameter is the discount negotiated and agreed upon. Sellers will generally try to offer discounts to attract customers while balancing the same against his profitability. Buyers, on the other hand, will always try to negotiate higher discounts before concluding their purchase transaction.